“There is no way we could do that,” exclaimed a colleague upon hearing that Vanderbilt University, Nashville, was transitioning to generally accepted accounting principles budgeting. Shifting to a GAAP perspective for budgeting and managing departmental, school, and unit results was a five-year process at Vanderbilt. As one can imagine, the transition created a lot of skepticism, anxiety, and confusion.

Traditionally, nonprofits, colleges, and universities have leveraged fund accounting in order to manage funding allocations to faculty, programs, and departments, along with managing donor requirements. Meanwhile, the controller’s office translated those results into a GAAP format for external reporting. As a result, many institutions have been stuck between two worlds: internally managing and tracking resources through fund accounting, while also presenting external financial reports in GAAP. This ongoing conversion of financial results creates a continual disconnect between real financial activity and the understanding of local schools and units of their true operating results.

Following a confluence of issues that are discussed in this article, Vanderbilt decided to simplify and align its internal financial management and external reporting. As the university’s financial leaders weaned themselves off their dependence on fund accounting, managing the change process included clearly defining terms, educating the community, adapting systems, aligning processes, and shepherding every individual change through different mediums and with different stakeholder groups. In addition to discussing the change process, this article outlines the purpose, phases, methods, outcomes, and lessons learned for Vanderbilt.

Originating Station

First, a word about where we started and how we arrived at our final destination. Historically, Vanderbilt based its internal management reporting on fund accounting principles. Fund accounting emphasizes accountability rather than profitability. The focus is on “fund balances” that are set aside to achieve a specific goal or purpose within the organization, such as current funds or unrestricted operating funds, restricted funds, plant funds for capital investments, debt service, agency funds, or internally designated funds.

As such, Vanderbilt’s internal reporting, using a fund accounting method, was in contrast to GAAP, on which the institution’s external financial reporting was based. GAAP principles, standards, and procedures focus on performance over a given period of time via the generation of an income statement and balance sheet. The reporting framework is as follows:

- Required statements (profit and loss, and balance sheets).

- Three net asset classifications: unrestricted (for any purpose), temporarily restricted (certain conditions such as time or purpose must be met), and permanently restricted (largely comprises the university’s endowment). Effective FY20, institutions will shift to having only two net asset classes: with restrictions and without restrictions.

- All expenses reported as unrestricted.

- Release of restrictions.

- Quasi/true endowment.

Because higher education institutions are required to report in accordance with GAAP, there is growing interest within the industry to align internal reporting and budgeting with external financial reporting. Many boards already advocate for this continuity.

Applying two different standards for internal and external reporting is problematic for many reasons, including a lack of clarity surrounding the performance of the institution and respective areas, inconsistent definitions of liquidity, and the availability of resources for internal distribution and strategic investments. This disconnect creates a lack of accountability across schools and support units when managing each unit’s individual performance, as well as the institution’s performance. To mitigate confusion among the university’s board of trust members, who largely operated in a GAAP world, Vanderbilt’s accounting department prepared two views of results each period—one based on the internal fund accounting view and the other which paralleled GAAP.

Preparation of two different views of results also required accounting to maintain a complicated translation of results between internal and external reporting that differed materially. A few of the differences resulted from areas utilizing internal transfers to bolster net results, centrally recording interest and depreciation, and challenges with internal eliminations of intracompany activity at the consolidated level.

Additionally, Vanderbilt’s homegrown reporting tool housed many adjustments required to translate the general ledger accounting records into GAAP financial statements. This tool and its output were available only to those in central finance. Therefore, individuals in operational areas did not have access to this GAAP information, other than the consolidated results published on a quarterly basis. Even as the university began its shift to GAAP reporting at the consolidated level, much of Vanderbilt’s internal reporting, such as results by area, remained rooted in the fund accounting view, thus preventing the full transition to GAAP reporting. This difference in presentation created an ongoing disconnect between the way management viewed consolidated results and how business officers viewed and managed their business.

To track availability of cash across the institution, our accounting department maintained a 200-plus-page fund balance report with cash and non-cash fund balances. Total cash fund balance included claims on cash by area, also known as “due to” and “due from,” as areas did not hold their own cash accounts, but rather had claim to dollars within the central university bank, as well as fund balances associated with assets and liabilities. Types of cash fund balances included operating, externally designated, internally designated, plant reserves, and plant projects claim on university bank assets. Non-cash fund balances included capital assets, depreciation, and other.

The chart of accounts (COA) added further complexity as each fund type was defined by a 10-digit center of four fields, with unique positions for type of fund, division, department number, and unique identifier. As of 2016, there were approximately 40,000 different centers across the institution.

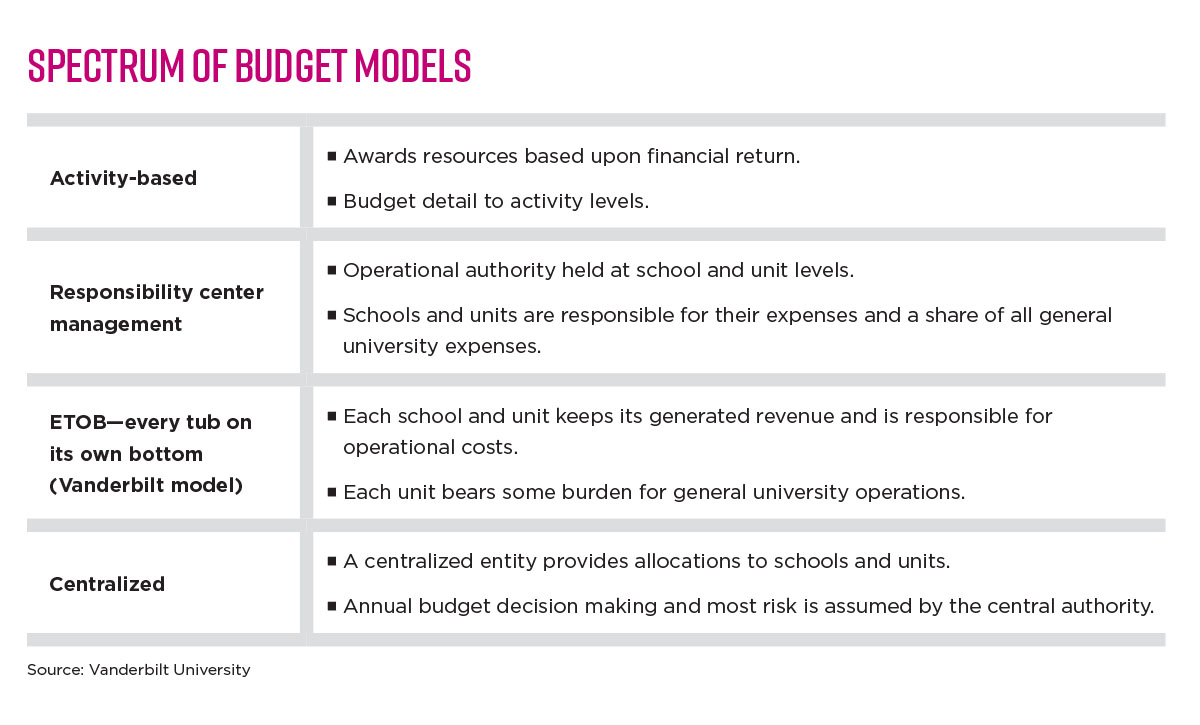

With such a disjointed approach to managing internal resources, it was the responsibility of central finance to manage results institutionally. And, with the added confusion resulting from two standards of reporting (internal—funds, and external—GAAP), there was a perceived lack of transparency of the university’s performance among faculty and staff, creating a distrust of the central administration. At about the same time, the institution undertook a slow transition from a centralized budget model to Vanderbilt’s version of responsibility center management—referred to as “every tub on its own bottom” (ETOB)—which shifted more accountability to individual areas.

In addition, two events facilitated Vanderbilt’s full conversion to a GAAP view for budgeting and internal reporting. First, the university reorganized its clinical operations into a separate not-for-profit (NFP) entity and medical center in April 2016, increasing scrutiny of university financial results and requiring us to establish certain barriers to prevent conflicts of interest. This included shifting the university’s general ledger off Vanderbilt University Medical Center’s application and server, which was legally required, as the ability to view VUMC financials and vice versa did not allow for appropriate segregations of duty under the new master transfer and separation agreement.

Second, the university experienced tremendous growth, while its finance and human resources systems remained stagnant. University leadership made the decision to shift from the 30-year-old mainframe technology to software as a service in the cloud. In FY18, the GAAP-based general ledger went live in support of the enterprise resource planning (ERP) integration effort of the general ledger, human resources, budgeting, grants, and procurement modules.

Destination Point

Reaching the final stop on our journey required addressing the impacts of GAAP budgeting and reporting, and securing campuswide adoption. Public and private institutions typically leverage a spectrum of different budget models, from decentralized to centralized. Over a five-year time period from FY14 to FY18, Vanderbilt undertook a robust resource alignment through the shift to ETOB reinforced by GAAP accounting principles.

To start, the university built a foundation by creating a committee to manage infrastructure costs, reviewing unexpended gift and endowment funds, and increasing its endowment payout policy.

Next, Vanderbilt aligned its fiscal policies with the ETOB model by lowering the capital bank rate to better align with external borrowing costs, directing facilities and administrative cost recoveries to schools, and aligning assets and depreciation with their respective areas.

Finally, the university recognized tuition revenues at the local unit level by distributing undergraduate tuition, as well as funded and unfunded financial aid, to the four undergraduate schools through a formula agreed on by the provost and deans.

Shifting to ETOB for budgeting and reporting established new allocations, which allowed for a proportionate distribution of university common-good expenses to each school and unit. This resulted in comprehensive area income statements and balance sheets, as well as internal eliminations at the consolidated level. Said another way, this ensured that areas contributed toward costs associated with running the university, while also directly recognizing the income earned by each respective area.

In addition to distributing undergraduate tuition, undergraduate financial aid endowment distributions, and facilities and administrative cost recoveries, we also established the following intracompany allocated expenses:

- Technology: includes desktop support; telecom, learning management system and classroom support; and media services support.

- Real estate: includes rental rates for university-owned buildings and a lease management rate for nonuniversity real estate lease facilitation/representation.

- Utility charges: include utilities, buildings and grounds services, custodial services, and funding of planned plant infrastructure capital expenditures.

- Administrative support fee: includes cost center organizations such as human resources, finance, general counsel, and other general administrative support areas within the university.

- Academic unit allocation: supports academic units and strategic investments utilized by all schools, including provost’s office and related initiatives, enrollment affairs, libraries, the dean of students, and other vice provost areas.

- Insurance: includes bundled insurance (vehicle, property, general liability, cyber liability, and pollution liability), medical professional liability, and unit-specific insurance.

In Vanderbilt’s new GAAP world for budgeting and internal reporting, the shift to ETOB brought transparency to earnings before depreciation and the availability of cash by clearly defining what belonged to each area while shifting accountability to the individual areas of the university to manage their profits and losses and balance sheets. Adopting a common financial language enabled Vanderbilt leadership to operate with an identical view of operating results, allowing leaders to spend more time focusing on the long-term strategy for the university and less time translating internal versus external reporting.

A quarterly review of each school’s and each unit’s core operating results, cash position, and operating margin provided a new focus on true financial outcomes and long-term cash reserves. Long-term planning and tracking of individual school and unit balance sheets increased scrutiny on cash available for current and future cash commitments to ensure long-term financial viability. This increased transparency assisted the provost and deans as they developed their faculty recruitment and retention strategies as well as capital investment and facility renewal plans.

Station Stops Along the Way

Several important challenges emerged throughout this transition. For instance, communicating the transition plan and articulating the impacts of the changes were critical. Likewise, involvement and sponsorship from leadership—including the chancellor, chief information officer, vice chancellor for administration, provost, chief financial officer, chief human resources officer, and the associate vice chancellor for assurance, risk and advisory services—was fundamental to the success of the transformation. The university’s shift to GAAP budgeting and the ETOB model ushered in a significant change in Vanderbilt’s culture, philosophy, and mindset.

For instance, GAAP changes included:

- Timing of revenue and expense recognition.

- Movement away from “holding” invoices until the next fiscal year when there are new resources.

- Focus on releases from restrictions and temporary restricted revenues at schools.

- Focus on accruals/deferrals (e.g., academic year faculty salary accruals).

- Distinction between capital versus operating expenditures.

- Distinction of debt service (separate interest versus principal).

- No more “topside” entries made by central accounting.

- No more transfers between funds.

- Among the changes resulting from transition to an ETOB model:

- Visibility into profitability by area (earnings before depreciation).

- Tuition recognition by school.

- Ownership of individual assets.

- Effects of depreciation on area profit-and-loss statements.

- Greater focus on allocations and methodology.

- Increased transparency and accountability.

- Help informing/reinforcing application of GAAP.

Leadership brought in the provost and deans early to discuss the shift to GAAP and ETOB, how this would impact each of them individually, and the advantages and disadvantages of adopting this methodology. Many revenue and expense recognition discussions occurred, including timing of tuition revenue deferrals, academic year faculty salary expense accruals, interest and principal debt payment entries, and how non-capitalized operating expenses on capital projects impacted current operating results.

Understanding Vanderbilt’s capitalization policy was critical to budgeting and forecasting in areas with active or upcoming capital projects. Leadership also provided an incentive as part of the transition: While depreciation is a non-cash entry, each school received a one-time cash deposit equivalent to its annual depreciation into its cash reserves. This created some positive momentum.

Communication in the form of annual operating budget guidelines outlined different types of revenues and expenses, and how they are budgeted based on universitywide assumptions. This provided an annual resource guide for the chief business officers and deans, steering them through the changes for the year and reminding them of the existing practices. Additionally, an annual budget kickoff meeting with budget owners, internal rate owners, central accounting, and the budget office further described the process, the assumptions, and answered questions in advance of the budget season.

Internal charges and transfers created an accounting challenge. Revenue was recognized with the unit that generated it. Internal transfers of support became cash reserve transfers and did not impact current year profit-and-loss results of individual units. This change required areas to contemplate their true impact on revenue as part of the university’s financial statements rather than including internal support or other internally eliminating activity. Additionally, expense transfers became very limited, encouraging any sharing of expenses to occur when the expense was recorded through the payment of the purchase order or travel and expense reports.

Diversion Route

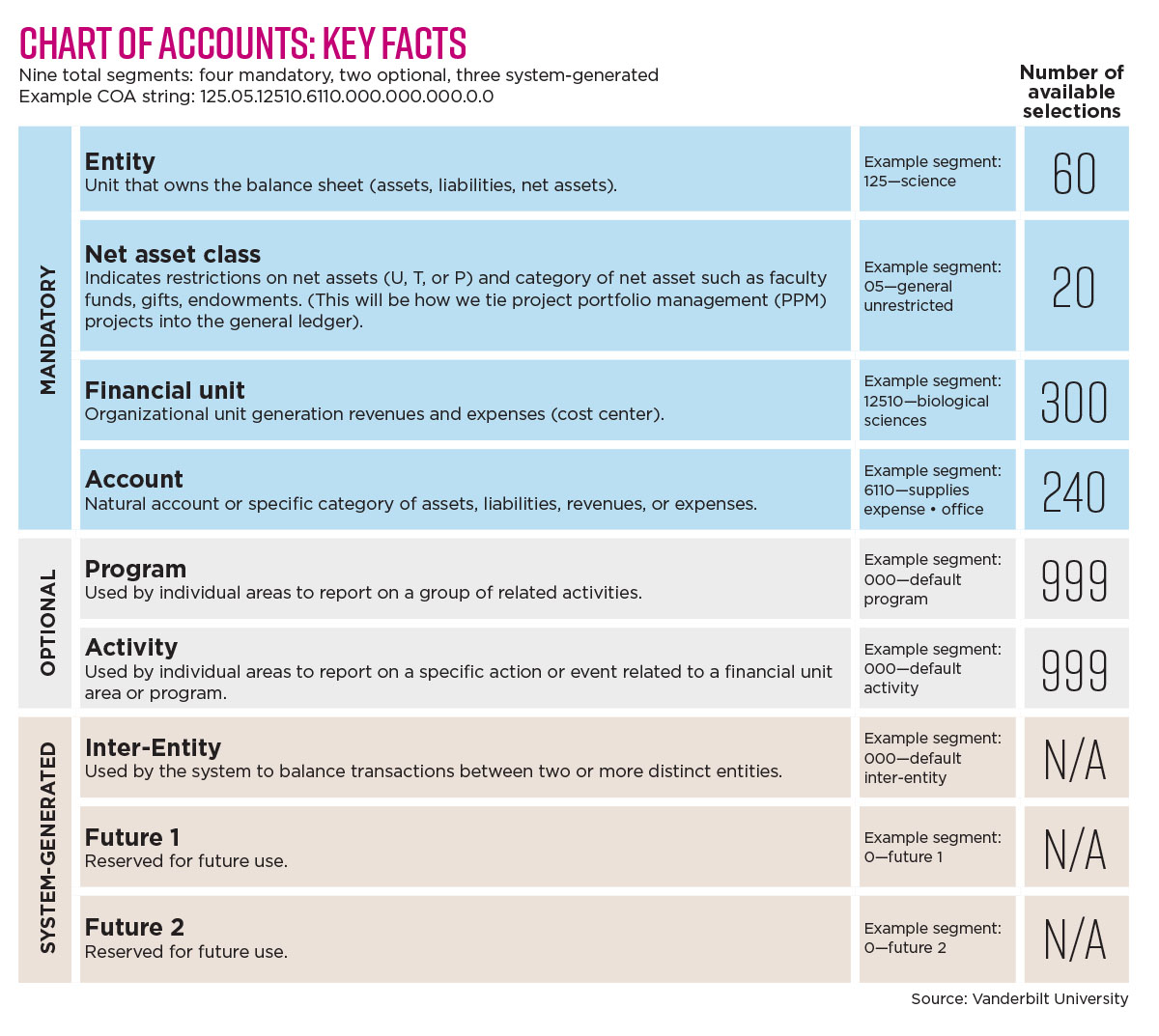

One key tool harnessed through the ERP implementation and shift to GAAP was a complete revision of Vanderbilt’s chart of accounts (COA). The new hierarchy included nine total segments: four mandatory, two optional, and three that were system-generated (see sidebar, “Chart of Accounts: Key Facts”). Among the mandatory segments was the entity or unit that owned the balance sheet. Balance sheets at the entity level supported GAAP by making the units more directly responsible for their own cash balances and by ensuring that areas understood the interactions between their profits and losses and balance sheets. Another mandatory segment was the natural account, or specific category of assets, liabilities, revenues, or expenses.

NACUBO’s Financial Accounting and Reporting Manual (FARM) for higher education contains a functional classification that provides standard definitions of mission-related activities across institutions. However, through the COA redesign, Vanderbilt was intentional in not creating a unique field to denote functional account categories. The university does not represent functional categories on the face of its financial statements. When external financial reporting requires a functional classification view of expenses, the new COA effectively supports an analytical approach to serve those reporting needs. The functional classification occurs through analyzing and organizing a combination of multiple attributes within the COA rather than one specific attribute.

The COA redesign reduced complexity by going from more than 2,000 accounts down to fewer than 300, and aligning the hierarchy with financial statement line items. Furthermore, it enabled the general ledger to function as a general ledger and not as a sub-ledger with layers of detail and transaction descriptions. With such significant streamlining of the COA, two optional fields were made available to areas—program and activity—which could be defined locally to allow for granular tracking and reporting. For instance, where athletics historically used an account to track different types of ticket sales, it could now define a program for a specific sport—and within that, an activity for a specific event—all while leveraging the same natural account for ticket revenue.

Additionally, following go-live, a robust reporting effort was undertaken to partner with areas in their operational, management, and close reporting needs. With the reduced COA and the perceived loss of reporting details, cooperation with leadership was crucial, collectively agreeing that reporting and data were available at a higher level.

Through the transition, CBOs developed a better understanding of the COA, accounting principles, and balance sheet activity. With a phased approach to the implementation over a five-year period, each accounting treatment was highlighted, reviewed, and discussed as part of the annual budget process.

Not everything went smoothly. Confusion related to academic year faculty salary accruals created some inaccurate forecasts and much uncertainty in FY17. Net assets released from restrictions recognition by the local units also created confusion in FY18. This was primarily due to the system conversion and CBOs not clearly understanding what gifts were already released at conversion date versus what would be released with upcoming expenditures. Details such as these are important to communicate and clarify on a regular basis throughout the changeover, particularly with refinements to the methodologies.

Given the complexity and dramatic cultural change required for the shift to GAAP there were some missteps and gaps in communication, but the CBOs, deans, vice chancellors, and university leadership quickly adapted. GAAP budget reporting changed the way those with budget responsibilities viewed their resource allocation and expense accountability and resulted in the following successes:

- Greater accuracy in budgeting more closely, reflecting actual financial results.

- Lack of need for a complicated cross-walk process at the university level.

- Better grasp of cash and profit-and-loss impact among budget officers.

- Consistent board of trust reporting—budget, management and internal statement of activities.

- Change in mindset away from asking for central financial support.

- Increase in entrepreneurial pursuits through improved accountability.

- Improvement in communication with financial results and expectations.

- Focus on cash targets by areas by pushing university-level goals to the school level.

- Focus on areas where Vanderbilt needs improvement and system upgrades.

- Improvement in anticipation of risks.

How to Become a Conductor

Reflecting on our process and outcomes, Vanderbilt leadership learned several important lessons on its journey from fund accounting to GAAP budgeting that other institutions may find beneficial:

- While the project team worked to identify, communicate, and document changes, adjustments made during plan implementation were not always widely shared. The best intentions to communicate did not always address slight changes or adaptions of the procedures in the middle of the fiscal year. Some of the changes were in response to unintended consequences from the procedures or identifying process simplification measures.

As with any change, communication was critical, and utilizing multiple communication vehicles frequently helped reinforce the changes.

- The controller’s office, CBOs, budget office, and operating units required clear alignment in determining how to record transactions and report financial results. The general ledger system, including the chart of accounts, needed revisions to record activity at the local level. Reporting needed to adapt to the new chart, reflecting the bottom line to which the units were responsible and accountable.

This was true no matter whether the focus shifted to earnings before depreciation, net cash contribution, or net change in operating assets.

- This process can occur gradually or all at once. Vanderbilt implemented components of this methodology over the course of five years, but the primary shifts occurred over three fiscal years. An ERP implementation provided a clear finish line that propelled the university toward that goal.

Depending on your institution’s process adaptability, system agility, and cultural flexibility, the transition can occur at a pace that allows effective implementation.

- Board members more quickly comprehended budgets, interim progress reporting, and annual financial reports when presented in a GAAP format. This also simplified Vanderbilt’s board of trust meeting preparation and reduced complex explanations related to internal transfers of revenues and expenses.

All Aboard

If your institution is ready to align its budgeting and reporting with its financial statements, some initial steps may be in order to prepare for a successful transition. First, ensure that senior leadership is in full support of the process. There likely will be pushback when making such an impactful shift of financial perspectives, and leadership must be aligned when the resistance occurs.

Second, lean on the certified public accountants and controllers to provide guidance while educating CBOs and other financial operations staff. Third, critically assess the functionality of your accounting and budget systems. These systems must support the revised process and will need some adaptation. Fourth, discuss and develop a transparent plan with financial leaders, including the CBOs. Once the plan is in place, share the key points with the provost, vice chancellors and vice presidents, and deans. When academic leaders are engaged and informed, they are much more supportive of the implementation.

Finally, do not underestimate the project management and coordination requirements from beginning to end. Some transactions require more thought and consideration. The more informed and educated individuals are across campus, the fewer surprises occur when the transactions are recorded.

Once you heed the warning signals, consider jumping aboard with GAAP, because this train is about to leave the station. If you map your path to align budgeting and internal reporting with your financial statements, your board will thank you.

ERIC BYMASTER is associate vice chancellor for finance, and EVELYN CATE GALLETTI is director of capital planning, projects, and operations, Vanderbilt University, Nashville.